Heathrow's business case

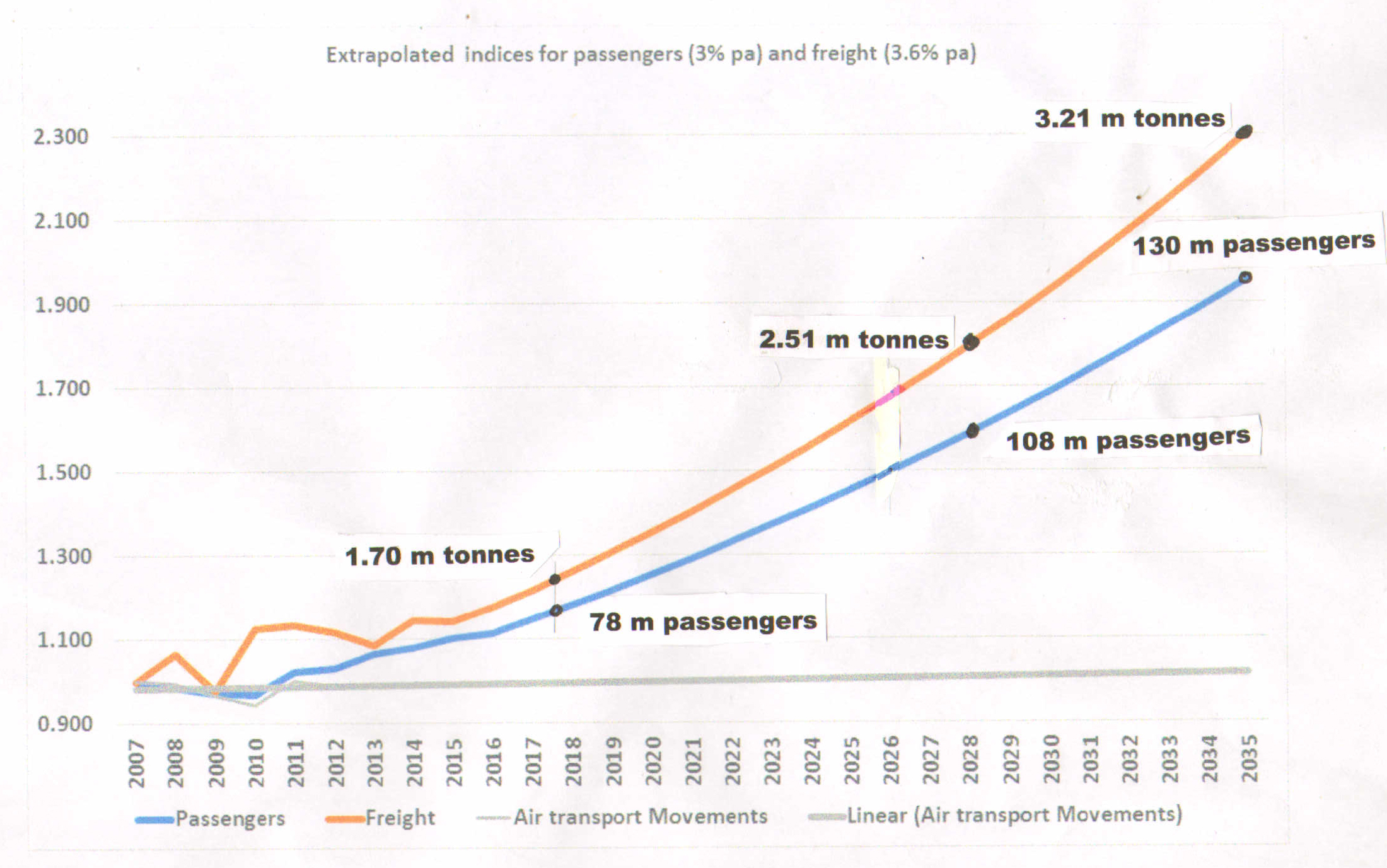

Doubling Heathrow's debt financing for its expansion with the runway cannot be achieved without a doubling of the airport charges. In any case, Heathrow's traffic is increasing - without the additional runway - with the progressive deployment of bigger aircraft. See the Heathrow indices plot, based on DfT's aviation statistics in, Figure 1 and the expanded indices plot in Figure 2. The indices are created by dividing the increasing traffic figures by those for 2007, when the number of its air traffic movements peaked and reached a maximum without night flights..

In Figure 2 a trendline from 2018 to 2035 has been added to the Heathrow indices plot in Figure 1. The progressive deployment of bigger aircraft is attaining a 3% increase a year in the number of passengers carried with the increase in the average number of passengers per flight.

Having already got the bigger aircraft, or having placed the orders for them, the airlines can simply select the size of aircraft deployed to match the numbers flying on a particular route. This is already happening, as with the restricted number of movements from 2007 to 2017, the number of passengers carried has increased by 14.7% (3% per year) and tonnage of freight by 21.7% (3.6% per year)

If the 3% increase a year continues, a 50% rise in passenger numbers to 108 million - without the runway - would be attained by 2028, by when it may or may not be built. The ultimate target of 130 million passengers a year would be attained by 2035, again without the runway.

The average number of passengers per flight can go up from 150 in 2007 and 175 in 2017 to 255 in 2028 and to 290 in 2035. The potential passenger numbers per year could go up from 68 million in 2007 and from 78 million carried in 2017, to 102 million in 2028 and to 130 million in 2035, depending on demand.

A further trendline has been added to the indices plot in Figure 2 for the increase in freight tonnages with a 3.6% rise per year, rising from 1.70 million tonnes in 2017, to 2.51 million tonnes by 2028 and 3.21 million tonnes by 2035.

The bigger aircraft are already in service or on order with investment by the airlines. In achieving the average number of passengers per flight needed, the bigger aircraft will compensate for the fewer seats in the smaller aircraft.

The traffic would only be restrained by the market for the expanded numbers and would require an expanded surface access. If the market grows with a reduction or restriction in airport charges, the ultimate traffic levels could be attained much earlier, assuming the current internal and external restraints are resolved.

To reduce the hours passengers spend in queues with border controls, Terminal 6, taken off the runway project to reduce its costs, is needed to handle the increasing number of passengers per flight and the additional freight in the wide-bodied passenger aircraft. To cope with the bigger, pure freight aircraft if deployed there would also need to be a bigger freight warehouse, also as the bigger passenger aircraft would handle more freight.

Rather than a piecemeal addition of supporting facilities and surface access, the scope of these facilities should be applicable to the ultimate passenger numbers of 130 million and freight tonnages of 3.21 million per year to avoid another round of expansion.

Airport and surface costs

In 2014 Jacobs, for the Airports Commission, estimated Terminal 6 to cost £3.34 billion and the associated piers and satelittes to cost £1.56 billion. With cost inflation and contingencies, the £4.80 billion total plus say £500 million for the freight warehouse could easily rise to £6-£7 billion in 2028 to 2035 when it will be needed, if not before. The road and rail connections should be specified to cater for the ultimate numbers as above. The surface access costs might well be £20 billion, but would be settled for the conceivable future.

Cost savings

The tunneling of the M25, the diversion of the peripheral roads, the demolition of the Lakeside EfW and IAG's Waterside HQ, the destruction of the Harmondsworth community and its church, schools, pubs and housing and the many unlisted hotels, factories and services would be avoided, the costs of which have never been adequately estimated. There is no published list of the affected premises.

Regional flights

The case for the runway has been based on the addition of more connections to regional airports, but this is not relevant to the business case for Heathrow. The bigger regional airports can readily add point-to-point long-haul flights to their destinations, avoiding the need for connections to Heathrow. The growing passenger queues are a disincentive for Heathrow, but an incentive for regional direct flights or for the use of competitive hubs.

Heathrow's business case

The fleets of bigger aircraft are already in service or on order, so Heathrow can simply with them match its growing business without the runway which is simply not needed. The ultimate limit of 130 million passengers a year was defined by Heathrow in its reports and prospectuses, but is probably realistic given the limits on the final capacity of its roads and rail connections.

The selection of the North West runway, with its tunnelling of the M25 and diversion of peripheral roads will limit access to and from the airport, reducing its revenue just when it needs to increase it to pay for the expansion. The cancelling of Terminal 6 to save expansion costs is ill-advised as the alterations to Terminals 2 and 5 instead will further add to queues and curtail revenue.

The expansion of Heathrow's business can be achieved by the continuous deployment of bigger aircraft while investing in better handling facilities for passengers and freight. The surface access has to match the progressive increase in traffic.

FGP Topco Limited

The financial state of FGP Topco Limited with its accumulated wealth in its multiple profit and loss reserves, its massive debt and tax avoidance, shows it is inappropriate for the expansion of such a vital part of the UK's infrastructure.

It could be temporarily nationalised into a transitional company with a prospectus for eventual plc status - as was BAA. The par value of FGP Topco's shares of £13.1 million may have a premium, but this could be discounted by the unwarranted dividends paid of £3.02 billion. The official receiver could then intervene to use its reserves to settle its debt, allowing a reestablished plc to raise sufficient equity to finance the airport facilities and surface access needed for its expanded traffic - without the building of the runway.

Figure 1

Figure 2

John Busby 8 July 2018